- Published on

Adaptation and Retrofitting

- Authors

- Name

- Jason R. Stevens, CFA

- linkedin@thinkjrs

Though our story began long before the pandemic, when it shut down the U.S. in March of 2020, the firm was deep in the middle-to-end of a nine-month financing journey to raise north of $500K. For what? It was our intention to invest directly in micro artists and discretionarily manage artist business expenditures that generate consumption.

Our Artist Platform artist tool was built by February of 2020, while Dan had already lined up twenty-five to fifty of our first artist cohort to take investments ranging from five hundred to five thousand dollar investment lots, apiece, depending on our initial qualitative and quantitative investment model. This model considered basic factors such as streaming consumption elasticity to relative market streaming consumption, presence and interaction on social media and other fan-consumption platforms, in addition to raw estimations of current and anticipated royalties. This model did not consider extreme value risks such as financial collapse, supply-chain collapse, or acts of God (or Governments) capable of entirely, though temporarily, removing a demanded industry from existence.

Given that the latter actually took place, we grew into those learnings. At that time we didn’t foresee the full-industry washout that would occur, until January of 2021 with full acceptance of live event dynamics in a now (almost) post-pandemic world. But backing up to the Spring and Summer of 2020, we truly believed that things would get back to normal within the year for everyday artists. Fortunately, we acted with prudence, regardless. Any reasonable operator should have seen, as we did, the severe financial consequences of not transitioning products to a digital-only focus. We were fortunate to make the choices we did, given our early stage within our firm lifecycle.

The firm quickly pivoted to this digital-only product strategy, releasing Fan.Booster, the predecessor for our music product brand b00st.com.

Proof and history are in the pudding. As I write this I’m proud to report we recently crossed our five hundredth b00st.com user, ads reached 20 million consumers, and we had over 25 thousand real views of b00st.com sites, profiles, and posts. Glimmering in our rearview mirror is the sullied artist investment paradigm we managed to pivot around, avoiding almost certain death. And in front of us a road full of opportunity, with vastly less negative financial and operational uncertainty.

Focusing on digital business

We began the firm’s fully-digital transformation during the week of March 7, 2020, having just returned from and canceled the rest of our seed round capital raising efforts. These were in-person in New York City and Los Angeles, with reputable artist institutions, music tech seed investors, and financial institutions, such as our venerable advisor, ACTIVIST, and the High yield desk of a major investment bank.

We transitioned the firm nearly overnight and refocused our Artist Platform Promo funding and consumption product development efforts towards a race to build an outer-facing digital advertising campaign product. Frankly, we had absolutely no idea how this would turn out. So we strategized from a financial standpoint, assuming our highest sunk cost was a messy intangible that overwhelmed the substance of nearly any other risk. The intangible on which we focused is best described as the joint expectation of the opportunity cost of development and the opportunity cost of not being at mass-market stage with our original Artist Platform thesis given that the live event market is/would be functioning.

Do not fret: our team spent little time assessing this option quantitatively, as it would entail estimating the joint, non-normal probabilities between normalcy in live-event dynamics, the success of our yet to-be created Fan.Booster product, and the potential size of market and success of our investing endeavors, given aforementioned normalcy. Fortunately for the reader, both analytical and empirical solutions to the expectation described above have been left as an exercise.

Qualitatively, the optimal strategy was fairly clear: target the broadest product niche in which our current technical assets could be deployed, autonomously, quickly, and in music, to hold the option of re-folding into our Artist Platform software. We figured that the worst outcome would be improvements in our core ad APIs along with a strategic capital raise to finance a return to our core artist investment mission, if the digital ad product were to fail commercially.

Fan.Booster

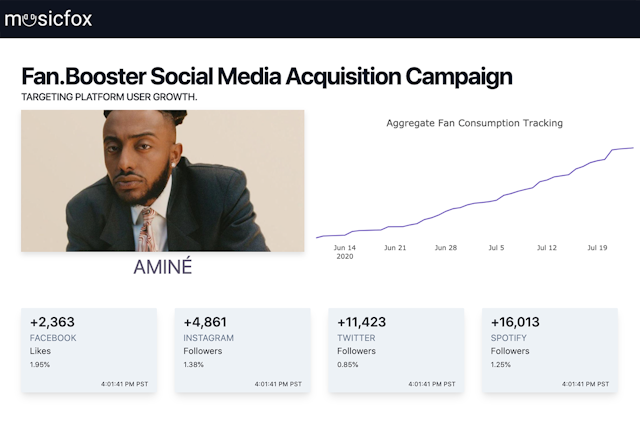

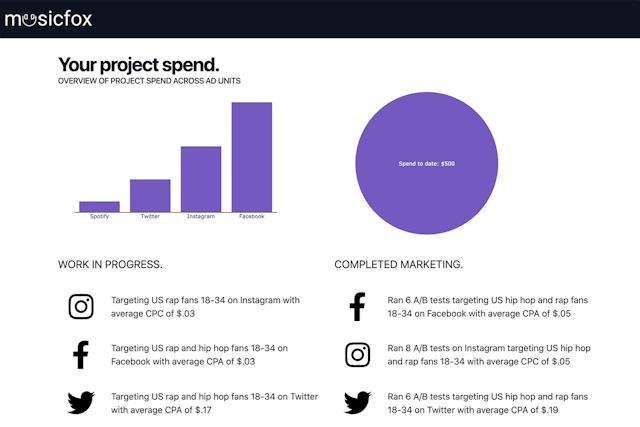

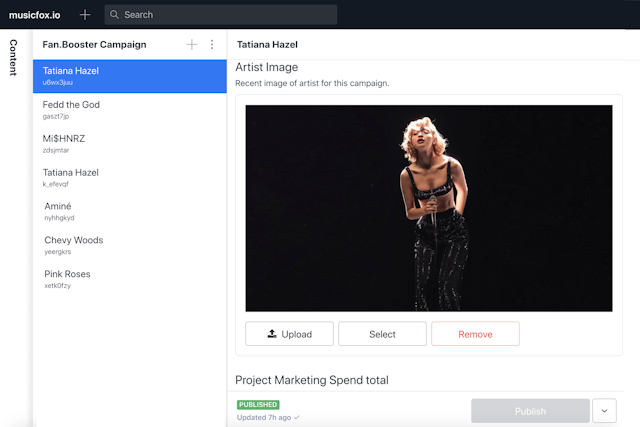

Fan.Booster campaign - Aminé; Internal content management application showing Tatiana Hazel’s campaign content from her initial onboard and ongoing updates.

Over the Spring and early summer the pandemic in 2020, your technical team of one managed to write a custom JavaScript frontend using the React framework, middleware server applications in JavaScript and Python, using automated pieces of our Python ad buying and reporting backend built for the Artist Platform. In addition, development included authentication, hyper-engineered marketing sites, internal content management applications and custom business management applications. Fan.Booster went into live production in May of 2020.

Meanwhile Phil and Dan quietly sold and worked Fan.Booster into major music reaching houses such as Taylor Gang, Downtown Records, and 300 Entertainment. For each artist they brought in, I ran our investment model in a Jupyter notebook covering thousands of touch points to result in a final ad channel allocation.

Over the proceeding nine months, we managed about forty boutique ad campaigns across a wide swath of artists big, small, and medium-sized, with the majority mostly unknown. Along the way we collected more than ten million price-interaction samples with ads on a minute-by-minute frequency through those first months. Fan.Booster artists were noted in Billboard Top-100 charts, several within the New York Times, the Chicago Tribune, and featured on top Spotify playlists, while running campaigns.

No longer an investment class, for us

Though we’ve never been close to the failure outcome as a business, we have substantially adjusted downward our investment opinions of the music industry and in particular, direct investability in the unknown-artist without access to a public balance sheet. A well-diversified portfolio of more than five-hundred upstart artists during and through the pandemic would have yielded negative relative returns to nearly any asset on the planet, as cash flows are almost perfectly correlated to live event interaction. We narrowly avoided the cost of our inability to comprehend a world in which that live event interaction would or could disappear.

Though a live-event extinction event as severe as the pandemic is unlikely to recur, the lack of a positive investible alternative to the small musical artist is unacceptable to this management team. As cash is dear in the underlying business of music, we will no longer be targeting direct investments in artists, outside of exceedingly rare and unique opportunities. We’re thankful now to have the gift of volition to ensure we do not subject our firm to these risks going forward.

In the process of discovering these facts while managing and building our first digital-only software product, we fell into a broader, unifying mission for the firm.